Opportunities, Risks, and Implementation Roadmap

Prepared with insights from WSO2, Chakray, and global banking modernization best practices.

1. Introduction

Central Asia’s banking sector is at a pivotal point. Digital payments, instant settlement systems, and super-app ecosystems are rapidly shifting consumer behavior, while regulators are opening the door to API-driven data sharing. For banks in Kazakhstan, Uzbekistan, and Kyrgyz Republic, modernization is not optional—it is an urgent necessity. An API-first strategy enables institutions to transform legacy cores into agile, modular service layers that can power new revenue streams, reduce integration costs, and extend their reach through ecosystems.

2. Regional Momentum

Kazakhstan is leading the charge with the National Bank of Kazakhstan’s Open API initiative and the roll-out of a single interoperable QR payment system. In 2024, over 85% of transactions were cashless (National Bank of Kazakhstan, 2024).

Uzbekistan’s Instant Payment System (IPS) demonstrates a rapid shift to digital payments, with a projected CAGR of 18% in non-cash volumes through 2027 (KPMG, 2024).

The Kyrgyz Republic processed 42.7 million QR transactions worth 48.8 billion soms by late 2024 (24.kg, 2024).

These shifts are further enabled by expanding 5G rollouts (GSMA, 2025) and rising financial inclusion, as highlighted in the World Bank Global Findex 2025 snapshots (World Bank, 2025).

3. Why API-First Matters

Globally, APIs are recognized as core business enablers. According to McKinsey, 88% of banking technology leaders report that APIs have grown in importance, with approximately 14% of IT budgets now allocated to API programs (McKinsey, 2023).

In the UK, Open Banking data shows 130 million API-based payments in 2023, representing a 90% year-on-year growth (Open Banking UK, 2024).

For Central Asia, the implication is clear: APIs are the bridge between bank rails and super-app ecosystems such as Kaspi. Without APIs, banks risk falling behind as consumers migrate toward seamless embedded finance experiences.

4. API-First in Practice

Adopting an API-first approach means designing banking capabilities as API products from day one. This requires a foundation of governance, security, lifecycle management, and developer enablement.

Banks must move beyond simple “bolt-on” integrations toward domain-driven microservices exposed through secure gateways. To achieve this, several key principles should guide implementation:

-

REST/JSON APIs with versioning and OpenAPI specifications.

-

OAuth2/OIDC aligned with FAPI (Financial-grade API) security profiles.

-

Consent management systems to ensure compliance with evolving privacy regulations.

-

Developer portals and sandboxes to drive external ecosystem adoption.

-

ISO 20022 schemas and extensible data models to prepare for future open finance alignment.

5. High-ROI Use Cases

Several practical, high-value use cases highlight the potential of API-first modernization:

-

Account-to-Account (A2A) Payments & QR: Leveraging IPS and national QR schemes for instant settlement.

-

Embedded Consumer Finance: APIs for eligibility, BNPL, and instant lending integrated with marketplaces.

-

SME Onboarding: Accelerating account opening and underwriting using consented data.

-

Cross-Border Remittances: Exposing FX and payout APIs to capture remittance inflows.

-

Micro-Savings & Deposits: Embedding savings products into gig economy and employer apps.

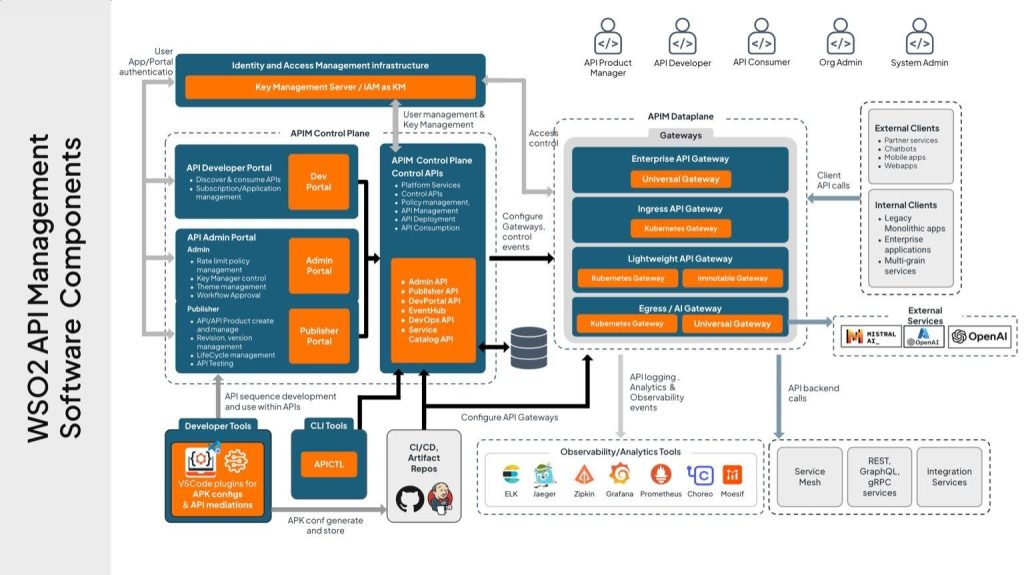

6. Reference Architecture

A modern API-first bank architecture consists of the following layers:

-

Experience layer

-

API management layer

-

Identity and consent layer

-

Domain microservices

-

Data and AI layer

-

Legacy core systems

Below is the reference architecture diagram:

WSO2 API Manager Architecture

7. Roadmap for Implementation

Wave 1 (0–6 months):

-

Establish API governance and product ownership.

-

Deploy WSO2 API Manager gateway, portal, and OIDC-based identity.

-

Launch lighthouse APIs (payments, onboarding).

Wave 2 (6–12 months):

-

Expand to analytics APIs and SME finance.

-

Monetize through tiered API packages.

-

Build developer ecosystems with sandboxes and hackathons.

8. Risk, Compliance, and Trust

Managing risk and compliance is critical in API-first modernization.

-

Consent-as-a-service must be implemented in alignment with FAPI (Financial-grade API) standards to ensure security and regulatory compliance.

-

Data localization laws in Uzbekistan, Kazakhstan, and the Kyrgyz Republic must guide architectural decisions, particularly around data residency and cloud deployments.

-

Banks should also provide transparent error handling and dispute resolution APIs to meet regulator requirements and uphold consumer trust.

9. Country Snapshots

- Kazakhstan: Focus on Open API readiness and QR/A2A.

- Uzbekistan: Leverage Instant Payment System (IPS)-native APIs for merchant services and SME lending.

- Kyrgyz Republic: Build APIs tailored for QR-heavy merchants and remittance payouts.

10. How WSO2 and Chakray Can Drive API-First Modernization

WSO2 provides the technical backbone for API-first modernization. Its API Manager offers a unified platform for API publishing, secure gateway traffic, consent management, analytics, and monetization. Combined with WSO2 Identity Server, banks can enforce OpenID Connect (OIDC) and FAPI standards.

Chakray acts as the consulting and delivery partner—guiding banks through strategy design, regulatory compliance, and phased implementation. With regional experience, Chakray can help banks tailor WSO2 deployments to Central Asian conditions, from integrating IPS to ensuring data residency compliance.

Together, WSO2 and Chakray can establish API Centers of Excellence, run partner onboarding programs, and deliver lighthouse projects with measurable ROI.

Below is the lifecycle flow diagram:

WSO2 Lifecycle Flow

11. Conclusion

An API-first strategy provides Central Asian banks with a pragmatic path to modernization. By exposing modular, secure, and monetizable APIs, banks can accelerate partnerships, capture embedded finance opportunities, and align with evolving regulatory regimes.

With WSO2’s proven technology stack and Chakray’s consulting expertise, banks can unlock double-digit cost savings and revenue growth, while shaping the future of finance in the region.

Ready to explore how API-first can transform your bank? Contact us to start your modernization journey today.

Talk to our experts!

Contact our team and discover the cutting-edge technologies that will empower your business.

contact usReferences

-

National Bank of Kazakhstan – Open API Initiative

-

GSMA – 5G and Connectivity

-

World Bank – Global Findex Database

-

McKinsey – API Survey

-

UK Open Banking – Usage Statistics

-

WSO2 Documentation – API Manager Architecture